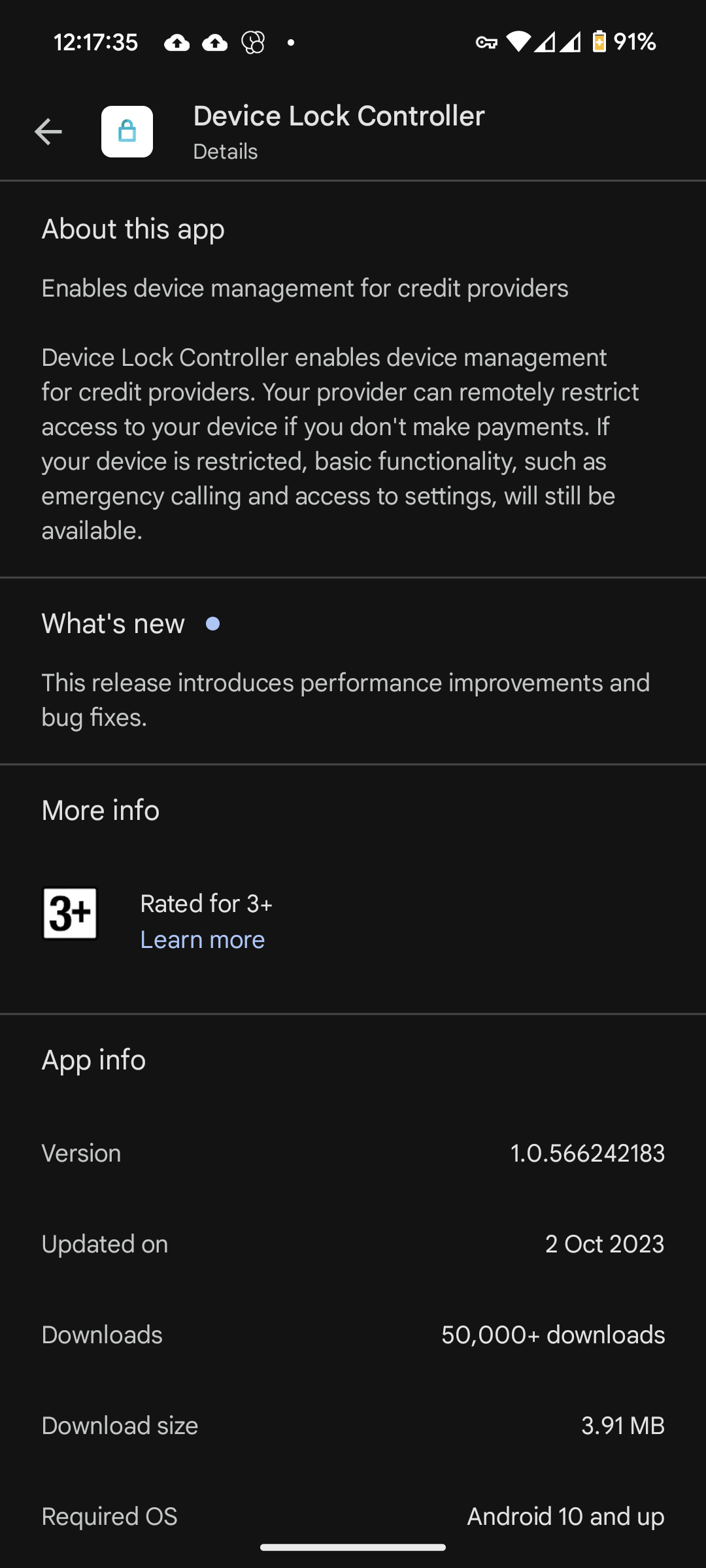

I installed NetGuard about a month ago and blocked all internet to apps, unless

they’re on a whitelist. No notifications from this particular system app (that

can’t be disabled) until recently when it started making internet connection

requests to google servers. Does anyone know when this became a thing? Edit 2: I

bought my Pixel 6 phone outright, directly from Google’s Australian store. I

have no creditors. Were the courts not enough control for creditors? Since when

are they allowed to lock you out of your purchased property without a court

order? I don’t even live in the US, so what the actual fuck? Edit 1: You can

check it’s installed (stock Pixel 6 android 14) Settings > Apps > All Apps >

three dot menu, Show system > search “DeviceLockController”. I highly recommend

getting NetGuard, you can enable pro features via their website if you have the

APK for as low as 0.10€, but donate more, because it’s amazing. You can also

purchase via Google Play store.

Everyone in this thread is wild. Buying a phone on credit makes sense with how expensive they are. How else can Google protect themselves though? Just like cars get repossessed if you didn’t pay, this is a two-way street. Otherwise people could have a phone sent to them and then never pay anything for it.

If the creditor wants to collect on a debt, there is a court process for that. I’ve used it. It works.

Locking the phone is not repossession. It does nothing other than sabotage the device the consumer may need to actually make the payment. The phone remains in the buyer’s possession and useless to the seller.

Power is also misplaced. What happens when the creditor decides to (illegally) refuse cash payments on the debt? Defaulting is not necessarily the debtor’s fault. This in fact happened to me: Creditor refused my cash payment and dragged me into court for delinquency. Judge ruled in my favor because cash acceptance is an obligation. But this law is being disregarded by creditors all over. If the creditor had the option to sabotage my lifestyle by blocking communication and computing access, it would have been a greater injustice.

I guess a closer analogy would be rental storage. If you don’t pay your mini storage bill, in some regions the landlord will confiscate your property, holding it hostage until you pay. And if that fails, they’ll even auction off your contents.

So in the case at hand the creditor is holding the debtor’s data hostage. One difference is that the data has no value to the creditor and is not in the creditor’s possession. It would be interesting to know if the contracts in place legally designate the data as the creditor’s property. If not, the data remains the property of the consumer.

This is covered by human rights law. Universal Declaration of Human Rights, Article 17 ¶2:

“No one shall be arbitrarily deprived of his property.”

If the phone user did not sign off on repossession of their data, and thus the data remains their property, then the above-quoted human right is violated in the OP’s scenario.

He presented his logic and included well-recognised definitions and sources. He literally could not have done better without a peer review in the field 🤣🤣

Don’t try to strawman this. Human rights are violated when someone is deprived of their property (their data in the case at hand). If food is withheld from starving people in Gaza, your argument is like saying:

“Claims human rights are being violated because someone failed to drive a truck”

They’re not at odds. We don’t have to choose between protecting UDHR Art.3 and Art.17. It’s foolish to disregard some portion of the UDHR needlessly and arbitrarily.

I agree that this makes sense in the context of a creditor securing a loan, but I disagree that getting your phones on credit makes sense.

New, flagship devices can be had around $500 US, which is attainable for most Americans in a fairly short timeframe. Spending years locked into a carrier contract where you don’t own your device just doesn’t make sense unless you’re spending thousands on a foldable device or something.

For people who know as much about technology as most people in this discussion the thing to do if short of cash would be to buy a cheaper phone. I recently got myself a quite decent Note9 for $109AU and I could have got something even cheaper if I needed to. But many people aren’t as well informed, the above article is one example of people who are less well off being scammed by a corporation.

Everyone in this thread is wild. Buying a phone on credit makes sense with how expensive they are. How else can Google protect themselves though? Just like cars get repossessed if you didn’t pay, this is a two-way street. Otherwise people could have a phone sent to them and then never pay anything for it.

If the creditor wants to collect on a debt, there is a court process for that. I’ve used it. It works.

Locking the phone is not repossession. It does nothing other than sabotage the device the consumer may need to actually make the payment. The phone remains in the buyer’s possession and useless to the seller.

Power is also misplaced. What happens when the creditor decides to (illegally) refuse cash payments on the debt? Defaulting is not necessarily the debtor’s fault. This in fact happened to me: Creditor refused my cash payment and dragged me into court for delinquency. Judge ruled in my favor because cash acceptance is an obligation. But this law is being disregarded by creditors all over. If the creditor had the option to sabotage my lifestyle by blocking communication and computing access, it would have been a greater injustice.

#WarOnCash

I guess a closer analogy would be rental storage. If you don’t pay your mini storage bill, in some regions the landlord will confiscate your property, holding it hostage until you pay. And if that fails, they’ll even auction off your contents.

So in the case at hand the creditor is holding the debtor’s data hostage. One difference is that the data has no value to the creditor and is not in the creditor’s possession. It would be interesting to know if the contracts in place legally designate the data as the creditor’s property. If not, the data remains the property of the consumer.

This is covered by human rights law. Universal Declaration of Human Rights, Article 17 ¶2:

If the phone user did not sign off on repossession of their data, and thus the data remains their property, then the above-quoted human right is violated in the OP’s scenario.

Lemmy moment. Claims human rights are being violated because smartphone gets locked

He presented his logic and included well-recognised definitions and sources. He literally could not have done better without a peer review in the field 🤣🤣

So: shut up bitch

Don’t try to strawman this. Human rights are violated when someone is deprived of their property (their data in the case at hand). If food is withheld from starving people in Gaza, your argument is like saying:

“Claims human rights are being violated because someone failed to drive a truck”

Someone not paying a phone bill doesn’t equate to someone bombing Israel

They’re not at odds. We don’t have to choose between protecting UDHR Art.3 and Art.17. It’s foolish to disregard some portion of the UDHR needlessly and arbitrarily.

I agree that this makes sense in the context of a creditor securing a loan, but I disagree that getting your phones on credit makes sense.

New, flagship devices can be had around $500 US, which is attainable for most Americans in a fairly short timeframe. Spending years locked into a carrier contract where you don’t own your device just doesn’t make sense unless you’re spending thousands on a foldable device or something.

This is a frankly deranged take considering that 40% of americans dont even have the funds to save for a $400 emergency as of May 2023

https://www.accc.gov.au/media-release/telstra-to-pay-50m-penalty-for-unconscionable-sales-to-indigenous-consumers

For people who know as much about technology as most people in this discussion the thing to do if short of cash would be to buy a cheaper phone. I recently got myself a quite decent Note9 for $109AU and I could have got something even cheaper if I needed to. But many people aren’t as well informed, the above article is one example of people who are less well off being scammed by a corporation.